Dealer financing is a loan arrangement where a car dealership acts as an intermediary between you and a lender, marking up the base interest rate to generate profit while facilitating your vehicle purchase. Known formally as indirect lending, this process covers the majority of new-car loans in the United States. Understanding how dealer financing works before you walk into a showroom gives you real negotiating power and protects you from paying more than necessary.

How does dealer financing work?

Indirect lending dealer financing is the primary method for most new-car loans in the U.S., allowing buyers to complete a vehicle purchase and secure financing in a single dealership visit. The dealer originates the loan, then sells it on the secondary market to a bank or credit union. You never deal directly with the lender during the purchase process.

The mechanics are straightforward. You fill out a credit application at the dealership. The finance and insurance (F&I) office submits that application to multiple lenders at once, collects competing offers, and presents you with a single set of loan terms. Once you sign the Retail Installment Contract, the loan is assigned to the winning lender. After that point, all loan servicing transfers to the lender, and the dealer steps out of the picture entirely.

The key term to understand is the "buy rate." That is the raw interest rate the lender quotes to the dealer. The dealer then marks up that rate before presenting it to you. The difference between the buy rate and your final rate is the dealer's profit on the financing, called the dealer reserve.

How do dealerships find and offer financing options?

Dealerships work with two categories of lenders: captive lenders and third-party lenders. Captive lenders are financing arms owned by manufacturers, such as Ford Motor Credit or Toyota Financial Services. Third-party lenders include banks, credit unions, and independent finance companies. The F&I office submits your application to whichever lenders are most likely to approve your profile.

Dealerships submit credit applications to multiple lenders simultaneously, often enabling same-day approvals. Loan terms commonly range between 36 and 72 months. Longer terms lower your monthly payment but increase the total interest you pay over the life of the loan.

Lenders evaluate several factors when reviewing your application:

- Credit score and payment history

- Debt-to-income ratio

- Employment status and income verification

- Loan-to-value ratio of the vehicle

- Down payment amount

The speed of this process is a genuine advantage. Rather than visiting three separate banks before buying, you get multiple competing offers resolved in one sitting. That convenience has real value, especially when you need a vehicle quickly.

Pro Tip: Ask the F&I manager how many lenders they submitted your application to. A dealer with a wide lender network gives you better odds of a competitive rate, especially if your credit history is mixed.

What are dealer reserve and interest rate markups?

Dealer reserve is the markup a dealer adds to the lender's buy rate before presenting the loan to you. Dealers add a 0–3% markup to the buy rate, which can increase your total loan cost by hundreds or thousands of dollars. The markup is not disclosed separately on your contract. You only see the final annual percentage rate (APR), not the buy rate underneath it.

The dollar impact is significant. A 1.5% markup on a $30,000 five-year loan adds approximately $1,200 to your total repayment. That is money that goes directly to the dealership's F&I department, not toward your vehicle.

| Loan Amount | Markup Added | Loan Term | Estimated Extra Cost |

|---|---|---|---|

| $30,000 | 1.5% | 60 months | ~$1,200 |

| $30,000 | 3.0% | 60 months | ~$2,400 |

| $20,000 | 1.5% | 60 months | ~$800 |

| $20,000 | 3.0% | 60 months | ~$1,600 |

The F&I department is the most profitable section of most dealerships, earning an average of $1,500 to $3,000 or more per transaction through financing markups and add-on products. That profit incentive means the F&I manager is motivated to present the highest rate you will accept, not the lowest rate you qualify for.

Pro Tip: Request your credit score before visiting any dealership. Knowing your score lets you research realistic rate ranges on sites like Bankrate or NerdWallet, so you can recognize when a dealer's offered rate is above market.

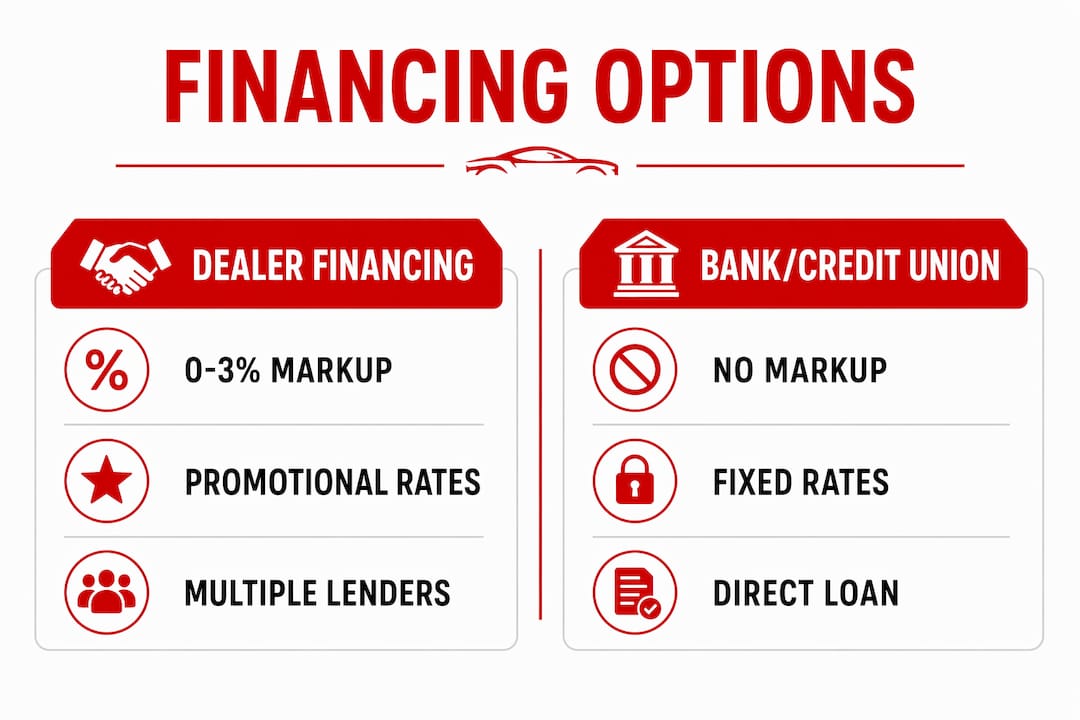

How does dealer financing compare to bank or credit union financing?

Direct financing means you secure a loan from a bank or credit union before visiting the dealership. The rate is fixed, there is no markup, and you arrive knowing exactly what you can afford. Dealer financing offers convenience and access to manufacturer promotions, but often costs more due to the reserve markup.

| Feature | Dealer Financing | Direct Bank/Credit Union |

|---|---|---|

| Rate markup | Yes (0–3%) | No markup |

| Speed of approval | Same day, often in hours | 1–3 business days typically |

| Manufacturer promotions | Yes (0% APR offers available) | Not available |

| Negotiation flexibility | Rate can be negotiated | Rate is fixed at approval |

| Credit score impact | Multiple lender pulls (bundled) | Single hard inquiry |

The strongest argument for dealer financing is access to manufacturer promotional rates, sometimes as low as 0% APR, available only through captive lenders. These subvented rates can outweigh any markup cost and represent genuine savings. A 0% APR offer on a $25,000 vehicle saves thousands compared to even a modest bank rate.

The strongest argument against dealer financing is the lack of transparency. You cannot see the buy rate, so you cannot calculate the markup. The best counter to this is arriving with a pre-approved bank offer. That gives you a concrete baseline rate and forces the dealer to compete with a real number.

Key situations where dealer financing wins:

- Manufacturer is offering 0% or sub-2% APR promotions

- You have strong credit and qualify for the best captive lender tiers

- You need same-day approval and cannot wait for bank processing

- The dealership has a wide lender network that includes credit unions

Key situations where direct financing wins:

- You have time to shop rates before buying

- Your credit is fair and you want to avoid markup on an already elevated rate

- You want full transparency on your loan terms before signing

What is "buy here, pay here" financing and who should consider it?

"Buy here, pay here" (BHPH) financing is a fundamentally different arrangement from standard dealer financing. The dealer does not submit your application to outside lenders. Instead, the dealership holds the loan itself and collects your payments directly. There is no third-party lender involved.

BHPH programs serve buyers with FICO scores below 500 who cannot qualify for standard financing. Interest rates on these loans often exceed 20% APR. That rate reflects the high default risk the dealer absorbs by lending to buyers with very limited credit history.

BHPH dealers often install GPS tracking devices or remote ignition disablers on vehicles. These tools allow the dealer to locate or disable the car if payments stop. That level of control is a direct consequence of the dealer carrying the loan risk.

BHPH financing is a last-resort option, not a preferred path. The difference between indirect lending and in-house BHPH financing is significant in terms of loan ownership, interest cost, and risk controls. If you are working with limited credit, exploring low income car financing options or credit-builder loans before committing to BHPH can save you thousands over the loan term.

Buyers who benefit most from BHPH financing share these characteristics:

- FICO scores below 500 with no path to traditional approval

- No co-signer available

- Immediate transportation need with no time to rebuild credit first

- Ability to make consistent on-time payments to rebuild credit history

Key Takeaways

Dealer financing works through a markup system where the dealership profits on the spread between the lender's buy rate and your final APR, making pre-approval your strongest negotiating tool.

| Point | Details |

|---|---|

| Dealer reserve markup | Dealers add 0–3% to the lender's buy rate, costing buyers up to $2,400 extra on a $30,000 loan. |

| Multi-lender submission | Dealers submit to multiple lenders at once, enabling same-day approvals with terms from 36 to 72 months. |

| Manufacturer promotions | Captive lenders offer rates as low as 0% APR, available only through dealer financing channels. |

| Pre-approval as leverage | Arriving with a bank pre-approval forces the dealer to compete with a concrete rate, reducing markup risk. |

| BHPH is a last resort | Buy here, pay here loans exceed 20% APR and are designed for buyers with FICO scores below 500. |

What I've learned from watching buyers navigate dealer financing

After working with car buyers across Providence and Rhode Island, one pattern stands out clearly. Buyers who arrive without a pre-approved rate consistently pay more. Not because dealers are dishonest by default, but because the F&I office has no incentive to offer the lowest rate when you have no comparison point. The markup system is legal, disclosed in the contract's APR, and entirely avoidable if you do your homework first.

The second thing I have seen trip buyers up is confusing a low monthly payment with a good deal. A 72-month loan at a marked-up rate can feel affordable month to month while costing $3,000 more than a 48-month loan at a lower rate. Always calculate the total repayment amount, not just the monthly figure.

Manufacturer promotional rates are the one scenario where dealer financing genuinely beats direct lending. A 0% APR offer from a captive lender is real money saved. The mistake buyers make is assuming that promotional rate applies to every vehicle on the lot. It typically applies only to specific models, trim levels, and credit tiers. Confirm eligibility before you build your budget around it.

The F&I office is designed to maximize profit through rate markups and add-on product sales. That is not a criticism. It is a fact you should factor into every conversation in that room. Go in informed, bring your pre-approval, and treat the financing negotiation as a separate transaction from the vehicle price.

— Elmwood

Financing options at Elmwoodautosalesri

Elmwoodautosalesri works with buyers across all credit profiles, from strong credit to bad credit car buying situations, to find financing that fits. Every vehicle on the lot goes through a thorough inspection before it is offered for sale, so you are financing a car you can trust.

Elmwoodautosalesri's Digital Retail platform, powered by Capital One, lets you explore financing options online before you ever set foot in the dealership. You can review real loan terms, estimate monthly payments, and arrive at the dealership with clarity on your budget. The process is transparent, low-pressure, and built around your schedule. Visit Elmwoodautosalesri in Providence, RI, or start your application online today.

FAQ

What is dealer financing in simple terms?

Dealer financing is when a car dealership arranges a loan on your behalf through a third-party lender, acting as an intermediary. The dealer submits your credit application to multiple lenders and presents you with the approved loan terms.

How does the dealer make money on financing?

The dealer marks up the lender's base interest rate, called the buy rate, by 0–3%. That markup, known as dealer reserve, is built into your APR and is not separately disclosed on your contract.

Is dealer financing better than going through a bank?

Dealer financing is better when manufacturers offer promotional rates as low as 0% APR through captive lenders. Direct bank financing is better when you want full rate transparency and no markup risk.

What credit score do I need for dealer financing?

Standard dealer financing typically requires a FICO score above 500. Buyers below that threshold may only qualify for buy here, pay here programs, which carry interest rates that often exceed 20% APR.

Can I negotiate the interest rate with a dealer?

Yes. Arriving with a pre-approved rate from a bank or credit union gives you a baseline that the dealer must beat to earn your financing business. That comparison forces the F&I office to offer a more competitive rate.