Low income car financing options are structured loan programs designed to help buyers with limited income or damaged credit secure reliable transportation at manageable monthly payments. Programs from lenders like People Driven Credit Union, Lacasa, and Freedom First Credit Union prove that a low credit score is not an automatic disqualification. The right program, combined with honest budgeting and proper documentation, puts a dependable used vehicle within reach for most households. Understanding which path fits your situation is the first step toward getting approved.

What financing options are available for low-income and credit-challenged buyers?

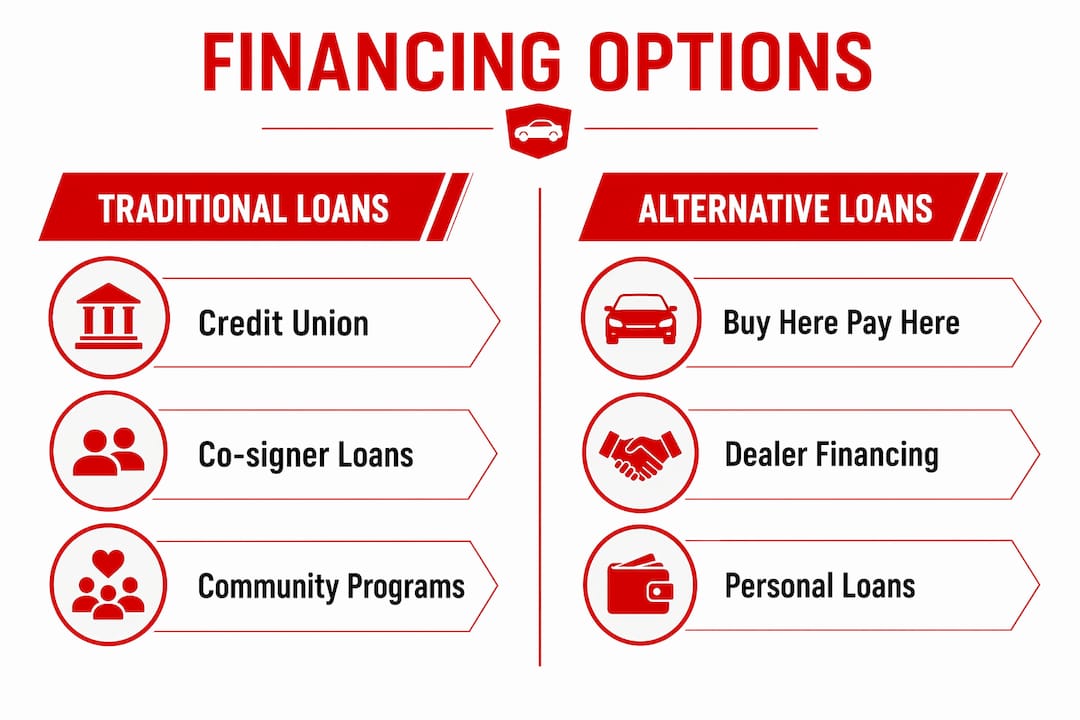

Affordable car loans for low-income buyers fall into four main categories: credit union loans, Buy Here Pay Here dealerships, community lending programs with financial coaching, and co-signer loans. Each serves a different financial profile, and knowing the differences saves you time and money.

Credit unions consistently offer the most competitive rates. People Driven Credit Union advertises used car loan rates starting at 4.74% APR with terms up to 72 months, plus a 90-day no-payment option for new members. That rate is reserved for well-qualified borrowers, but credit unions evaluate membership history and character alongside credit scores, which gives low-income applicants a real advantage over traditional bank lending.

Buy Here Pay Here (BHPH) dealerships are the most accessible option for buyers with no credit or severe credit damage. The dealer acts as the lender, approving loans in-house and collecting weekly or biweekly payments directly. Approval rates are high, but interest rates are also high, often exceeding 20%. BHPH works best as a short-term solution when no other option exists, not as a long-term financing strategy.

Community lending programs represent the most underused resource for financing for low income buyers. Lacasa's auto loan program offers fixed-rate loans between $6,000 and $12,000 at 14% APR over four years to borrowers with credit scores at or below 600 and household income under $71,600. Applicants must reside in Elkhart or St. Joseph County, Indiana, but similar programs exist in many states through nonprofit housing and community development organizations. The fixed rate and built-in financial coaching reduce default risk and help borrowers build credit simultaneously.

Pro Tip: Ask any lender whether the advertised "as low as" APR requires autopay enrollment or a specific credit tier. The actual rate offered to you may be significantly higher than the headline number.

Co-signer loans allow a borrower with limited credit to apply alongside a creditworthy co-signer, typically a family member or close friend. The co-signer's credit profile lowers the lender's risk, which translates to a lower APR for the primary borrower. The trade-off is real: if you miss payments, the co-signer's credit suffers equally.

| Financing type | Best for | Typical APR range | Key requirement |

|---|---|---|---|

| Credit union loan | Members with some credit history | 4.74% to 18% | Membership eligibility |

| BHPH dealership | No credit or severe damage | 20% and above | Proof of income and residence |

| Community program (e.g., Lacasa) | Low income, credit score below 600 | Fixed 14% | Income cap, counseling completion |

| Co-signer loan | Limited credit with a trusted co-signer | Varies by co-signer's credit | Willing and qualified co-signer |

What documents and preparations improve your chance of getting approved?

Lenders evaluating low income auto loans look beyond the credit score. They want evidence that you can and will repay the loan. Assembling a lender-ready package before you apply signals reliability and speeds up the process.

The documents most programs require include:

- Proof of employment for at least 90 days: Recent pay stubs, employer contact information, or a letter from your employer confirming your position and start date.

- Proof of income consistency: Two to three months of bank statements showing regular deposits that align with your stated income.

- Valid driver's license: Current and not suspended. Some programs also require a clean driving record.

- Proof of full-coverage auto insurance: Many community lenders, including Freedom First Credit Union, require proof that you can obtain full-coverage insurance before finalizing the loan.

- Proof of stable address: A utility bill, lease agreement, or bank statement showing your current address for at least 90 days.

- Payment history for rent and utilities: These are not on your credit report by default, but presenting 12 months of on-time rent or utility payments as printed records gives lenders a credit proxy when your score is thin.

Community lending programs explicitly evaluate character and demonstrated ability to pay, not just the number on a credit report. This means your documentation package carries more weight than it would at a traditional bank.

Pro Tip: Organize all documents into a single folder, physical or digital, before contacting any lender. Applicants who arrive prepared close loans faster and project financial responsibility from the first interaction.

Some programs also require completion of a financial counseling session before approval. Freedom First Credit Union's Responsible Rides program caps loans at 18% APR and pairs borrowers with a credit counselor. This requirement is not a barrier. It is a benefit that helps you understand your loan terms and build a plan to improve your credit score over the loan period.

How to budget and choose the best loan terms for affordability

The Experian Car Affordability Calculator recommends keeping total car payments at or below 10% of your monthly take-home pay. That figure is the starting point, not the ceiling. Total transportation costs, including insurance, fuel, and maintenance, typically add 50% to 100% on top of the loan payment itself.

Here is a practical breakdown of what to include when calculating your true monthly car budget:

- Loan payment: The fixed monthly amount owed to the lender.

- Full-coverage insurance: Required by most lenders and typically ranges from $100 to $200 per month for used vehicles in Rhode Island.

- Fuel: Estimate based on your daily commute and the vehicle's fuel economy rating.

- Maintenance and repairs: Budget at least $50 to $100 per month for oil changes, tires, and unexpected repairs on a used vehicle.

- Registration and taxes: Annual costs that should be divided into a monthly figure for accurate budgeting.

APR and loan term length are the two variables with the greatest impact on what you actually pay. A $10,000 loan at 14% APR over 48 months costs roughly $2,900 in total interest. The same loan stretched to 72 months reduces the monthly payment but increases total interest paid by several hundred dollars. Shorter terms cost less overall. Longer terms protect monthly cash flow but increase the total price of the vehicle.

A larger down payment directly reduces the loan principal, which lowers both the monthly payment and total interest. Even $500 to $1,000 down makes a measurable difference on a $7,000 used car loan. If a BHPH dealer or community program allows it, prioritize putting money down before signing.

| Loan amount | APR | Term | Monthly payment | Total interest paid |

|---|---|---|---|---|

| $8,000 | 14% | 48 months | ~$219 | ~$2,500 |

| $8,000 | 14% | 72 months | ~$158 | ~$3,400 |

| $8,000 | 18% | 48 months | ~$235 | ~$3,280 |

| $8,000 | 18% | 72 months | ~$170 | ~$4,240 |

How to apply for low income car financing step by step

Applying for bad credit car financing is more structured than most buyers expect. Following a clear sequence prevents wasted applications and protects your credit score from unnecessary hard inquiries.

-

Check your credit report first. Pull your free report from AnnualCreditReport.com and dispute any errors before applying. Even one corrected error can move your score enough to qualify for a better rate.

-

Get pre-approved or pre-qualified before visiting a dealership. Contact your local credit union or a community lending program and ask about pre-qualification. This gives you a realistic borrowing limit and a rate benchmark without a hard credit pull in most cases.

-

Compare at least three offers. Evaluate credit union loans, any applicable community programs like Lacasa or Freedom First Credit Union, and BHPH options side by side. Compare the total cost of each loan, not just the monthly payment.

-

Choose a vehicle within your pre-approved amount. Do not let a salesperson talk you into a vehicle that exceeds your pre-approval. Stick to the number your budget supports, factoring in insurance and maintenance costs before committing.

-

Negotiate the vehicle price separately from the financing. Dealers sometimes bundle price and financing into a single negotiation to obscure the true cost. Agree on the vehicle price first, then discuss loan terms.

-

Review the loan agreement line by line before signing. Confirm the APR, total loan amount, term length, and any fees. Watch for add-ons like extended warranties or gap insurance that inflate the loan balance without your explicit request.

-

Understand payment deferral terms if offered. Interest accrues during no-payment deferral periods even when no payment is due. A 90-day deferral on a $9,000 loan at 14% APR adds roughly $315 to your balance before you make a single payment.

Common mistakes to avoid when financing as a low-income buyer

Most financing problems for low-income buyers are preventable. The errors below account for the majority of denied applications and unaffordable loans.

- Focusing only on the monthly payment. A low monthly payment on a long-term loan can mean paying thousands more over the life of the loan. Always calculate total interest paid.

- Assuming the advertised APR applies to you. Advertised rates like 4.74% APR are reserved for the most qualified borrowers. Expect a higher rate and plan your budget accordingly.

- Skipping required financial counseling. Programs like Freedom First Credit Union's Responsible Rides require counseling for approval. Skipping or delaying this step stalls the application.

- Ignoring employment verification requirements. Most community programs require 90 days of employment at your current job. Applying before you meet this threshold wastes time and results in denial.

- Underestimating insurance costs. Borrowers with limited credit often pay higher insurance premiums. Get an insurance quote before finalizing a vehicle choice to avoid a budget shortfall.

Buyers with credit scores below 600 typically face APRs exceeding 28% on standard auto loans. Specialized programs capping rates at 14% to 18% represent a significant financial advantage worth the extra preparation they require.

Key takeaways

The most effective low income car financing strategy combines a community lending program or credit union loan with thorough documentation, honest budgeting based on total transportation costs, and completion of any required financial counseling.

| Point | Details |

|---|---|

| Community programs offer real rate advantages | Programs like Lacasa cap rates at 14% APR versus 28% or more on standard bad credit loans. |

| Documentation determines approval | Proof of 90-day employment, stable address, and full-coverage insurance readiness are required by most community lenders. |

| Total cost beats monthly payment | Always calculate total interest paid over the loan term, not just the monthly figure, before signing. |

| Payment deferral has a hidden cost | Interest accrues during no-payment periods, increasing your loan balance before repayment begins. |

| Pre-approval protects your budget | Getting pre-qualified before visiting a dealership prevents overspending and gives you negotiating leverage. |

What I've learned about financing cars for low-income households

After working with buyers across a wide range of credit and income situations, the pattern is consistent: the buyers who succeed are the ones who prepare honestly, not the ones who hope a lender overlooks their situation. The documentation package matters more than most people realize. Arriving with 90 days of pay stubs, a bank statement, and proof that you can obtain insurance tells a lender something a credit score cannot. It says you are organized and serious.

The other thing I have seen repeatedly is buyers underestimating insurance costs. A buyer qualifies for a $9,000 loan on a reliable sedan, then discovers the insurance premium pushes their total monthly transportation cost past what their budget can support. The total ownership cost calculation is not optional. It is the difference between a loan that builds your credit and one that breaks your budget.

Community programs with financial coaching requirements are worth the extra steps. The counseling is not a hurdle. It is practical education that most buyers wish they had before their first car loan. At Elmwoodautosalesri, we see buyers who have completed these programs arrive more confident, ask better questions, and make smarter decisions about which vehicle fits their actual budget. That outcome is worth every extra day of preparation.

— Elmwood

Find affordable auto financing at Elmwoodautosalesri

Elmwoodautosalesri is a trusted used car dealership in Providence, RI, built around transparent pricing and financing options designed for real buyers, including those with limited credit or income. Every vehicle on the lot passes a thorough inspection before it is offered for sale, so you are not taking a risk on reliability.

Elmwoodautosalesri offers flexible financing options including Buy Here Pay Here solutions for buyers across the credit spectrum. You can explore inventory and start a financing inquiry online before setting foot in the dealership. No commission-based pressure, no surprises. Just straightforward help finding a reliable vehicle at a payment that fits your budget.

FAQ

What credit score do I need for low income car financing?

Many community lending programs approve borrowers with credit scores at or below 600. Lacasa's program, for example, specifically targets applicants with scores under 600 combined with income below $71,600.

What is a Buy Here Pay Here dealership?

A Buy Here Pay Here dealership acts as its own lender, approving loans in-house without a third-party bank. Approval is easier than traditional financing, but interest rates are typically higher, often above 20%.

How does financial coaching help with car loan approval?

Programs like Freedom First Credit Union's Responsible Rides require financial counseling as part of the approval process. Completing counseling demonstrates commitment to repayment and helps borrowers understand their loan terms, reducing default risk.

Does a 90-day payment deferral save me money?

A payment deferral delays your first payment but does not pause interest. Interest continues to accrue during the deferral period, which increases your total loan balance before repayment begins.

How much car can I afford on a low income?

Experian recommends keeping your total car payment at or below 10% of monthly take-home pay. Add insurance, fuel, and maintenance to that figure to calculate your true monthly transportation budget before choosing a vehicle.