Dealer financing is a loan arranged directly through a dealership, and it is the most common way Rhode Island residents finance vehicle purchases today. The industry term is "indirect lending," where the dealer acts as a middleman between you and a network of lenders. As of Q3 2025, 81% of new-car purchases in the U.S. involved financing. That number shows just how central dealership loans have become to the car buying process. For Rhode Island buyers, the appeal comes down to three things: speed, credit flexibility, and access to manufacturer promotions that no bank can match.

Why Rhode Island residents use dealer financing: the core advantages

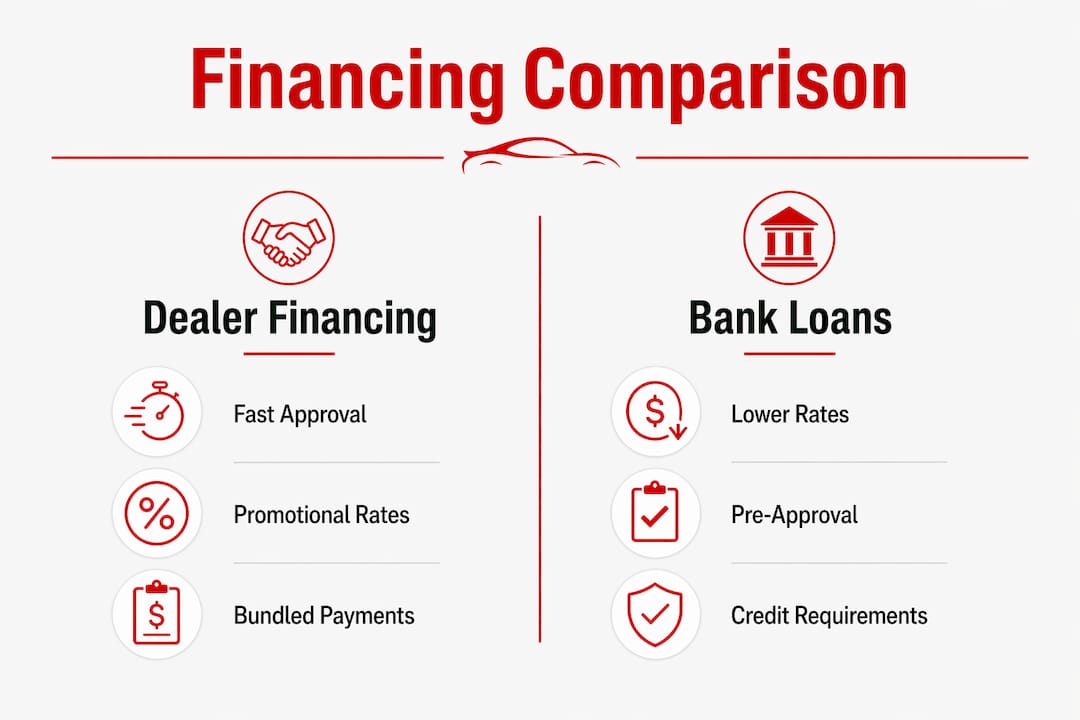

Dealer financing wins on convenience above everything else. You test drive a vehicle, agree on a price, and walk out with financing approved, all in one visit. No separate trip to a bank, no waiting several business days for a decision.

Speed is a real differentiator. Electronic platforms like DealerTrack allow dealers to submit loan applications to multiple lenders simultaneously and receive approvals within minutes. For a Rhode Island buyer who needs a car quickly, that same-day turnaround is a significant advantage over traditional bank timelines.

Manufacturer promotions are another benefit that only dealer financing can deliver. Automakers regularly offer subvented rates like 0% APR or promotional rates of 1.9% or 2.9% to move inventory. These rates are subsidized by the manufacturer and are not available through independent banks or credit unions. If you qualify, they represent the lowest possible cost of borrowing for a vehicle purchase.

Dealer financing also simplifies your monthly budget. Bundled monthly payments can include the vehicle price, an extended warranty, and GAP insurance in a single figure. That structure makes it easier to plan your monthly expenses without tracking multiple separate payments.

Pro Tip: Ask the finance manager specifically whether any manufacturer promotional rates apply to the vehicle you want. These offers change monthly and are not always advertised prominently on the lot.

How does dealer financing compare to bank or credit union loans?

The most important difference between dealer financing and a bank loan is who sets your interest rate. A bank gives you a fixed pre-approved rate based on your credit score. A dealer works with a lender's "buy rate" and then applies a markup of 0–3% on top of it. That markup generates $1,500–$3,000 in profit for the dealership per deal. Understanding this structure helps you negotiate more effectively.

Banks and credit unions typically require a FICO score of 660 or higher for standard approval. Dealer financing networks include specialized subprime lenders who work with scores below 600. That difference in access is significant for a large portion of Rhode Island buyers who fall outside the prime credit range.

The table below compares the two approaches across the factors that matter most to Rhode Island car buyers.

| Factor | Dealer financing | Bank or credit union loan |

|---|---|---|

| Approval speed | Minutes, often same day | 1–3 business days |

| Credit flexibility | Accepts scores below 600 | Typically requires 660+ |

| Manufacturer promotions | Available (0% APR, subvented rates) | Not available |

| Rate transparency | Markup applied above buy rate | Fixed pre-approved rate |

| Negotiation leverage | Bundled deal can obscure price | Separates price from financing |

| Add-on bundling | Warranty, GAP included in payment | Purchased separately |

The trade-off is real. Dealer financing bundles convenience with a potential rate markup. A bank pre-approval gives you a clear rate benchmark and separates the car price from the financing conversation. Neither option is universally better. The right choice depends on your credit profile, the available manufacturer promotions, and how quickly you need the vehicle.

Pro Tip: Get a pre-approval from your bank or credit union before visiting the dealership. You are not obligated to use it, but it gives you a concrete rate to compare against whatever the dealer offers.

What practical steps should Rhode Island buyers take before financing at a dealership?

Preparation separates buyers who get good deals from those who overpay. Follow these steps before you sign anything at a dealership.

-

Check your credit score. Pull your credit report from AnnualCreditReport.com before you shop. Knowing your FICO score tells you which lender tier you fall into and what rates are realistic for your situation.

-

Get pre-approved by a bank or credit union. A pre-approval letter gives you a rate benchmark. It also signals to the dealer that you are a serious buyer who understands financing. Use it as a negotiating tool, not a final commitment.

-

Research current manufacturer promotions. Automaker websites list current financing offers by model. If a 0% APR or low promotional rate applies to the vehicle you want, that offer is only available through dealer financing. Knowing this in advance prevents you from accepting a higher rate unnecessarily.

-

Keep your financing decision flexible. Signaling that you plan to pay cash upfront can reduce a dealer's willingness to negotiate on price. Keeping financing as an option on the table preserves your bargaining position throughout the negotiation.

-

Evaluate the total deal cost, not just the APR. A low monthly payment can hide a longer loan term or expensive add-ons. Calculate the total amount you will pay over the life of the loan, including any bundled warranty or GAP insurance, before agreeing to terms.

-

Ask about the buy rate. You can ask the finance manager what rate the lender approved you for before the dealer markup. Not every dealer will disclose this, but asking the question signals that you understand how the process works.

These steps apply whether you are buying a new vehicle or a used car in Rhode Island. The fundamentals of informed financing do not change based on vehicle age.

Why do Rhode Island residents with poor credit choose dealer financing?

Dealer financing is often the only practical path for Rhode Island buyers with damaged or limited credit. Banks and credit unions set strict minimum score requirements, and most decline applicants with recent bankruptcies, collections, or no credit history at all. Dealer networks operate differently.

Dealerships maintain relationships with specialized subprime lenders who accept applications from buyers with FICO scores below 600. These lenders price their loans to reflect higher risk, so interest rates are higher than prime rates. But approval is possible where a bank would say no.

The specific advantages for credit-challenged buyers include:

- Subprime lender access. Dealers submit your application to multiple lenders at once, increasing the chance of approval even with a low score.

- Recent bankruptcy acceptance. Some subprime lenders work with buyers who have completed a Chapter 7 or Chapter 13 bankruptcy, a situation most banks will not consider.

- Limited credit history options. First-time buyers or recent immigrants with thin credit files often qualify through dealer networks when traditional lenders decline them.

- Buy Here Pay Here availability. If standard dealer financing is not approved, a Buy Here Pay Here arrangement lets you finance directly through the dealership. Elmwoodautosalesri offers this option for buyers who need it. You can learn more about bad credit car buying options specific to Rhode Island.

- Speed when it matters. For buyers who need transportation immediately for work or family obligations, same-day approvals through dealer financing eliminate the waiting period that bank processes require.

Pro Tip: If you have a low credit score, bring proof of steady income and a larger down payment to the dealership. Both factors improve your approval odds and can reduce the interest rate a subprime lender offers.

Key Takeaways

Dealer financing gives Rhode Island residents the fastest, most flexible path to vehicle ownership, especially when manufacturer promotions or subprime credit situations are involved.

| Point | Details |

|---|---|

| Speed of approval | Electronic systems like DealerTrack deliver approvals in minutes, enabling same-day vehicle possession. |

| Manufacturer promotions | Rates like 0% APR are only available through dealer financing, not banks or credit unions. |

| Credit flexibility | Dealers work with subprime lenders who approve scores below 600 that banks typically reject. |

| Rate markup awareness | Dealers add 0–3% above the lender's buy rate, so comparing with a pre-approval protects you. |

| Total cost evaluation | Always calculate the full loan cost including add-ons, not just the monthly payment or APR. |

What I have learned about dealer financing in Rhode Island

After working with Rhode Island car buyers across a wide range of credit profiles, the biggest misconception I see is that dealer financing is always more expensive than a bank loan. That is simply not true. When a manufacturer is running a 0% APR promotion, no bank on the planet will beat that rate. The buyers who benefit most are the ones who did their homework before walking in.

The second thing I have learned is that most buyers negotiate the monthly payment instead of the total price. That is exactly what a dealer's finance office wants you to do. A longer loan term lowers your monthly payment while increasing the total amount you pay. Always anchor your negotiation to the out-the-door price first, then discuss financing terms separately.

Rhode Island's used car market is competitive, and timing matters. Manufacturer promotions typically run for 30-day windows tied to model year changeovers or sales targets. If you see a strong promotional rate on a vehicle you want, waiting a month to "think about it" often means the offer is gone. Preparation and timing together are what separate a good deal from a great one.

At Elmwoodautosalesri, we do not use commission-based sales tactics. That means our finance conversations are straightforward. We tell you what the lender approved, what options are available, and what the total cost looks like. You make the decision with full information.

— Elmwood

Financing options at Elmwoodautosalesri in Providence

Rhode Island buyers looking for transparent, pressure-free financing have a direct option at Elmwoodautosalesri in Providence. Whether your credit is excellent, limited, or recovering, the dealership works with multiple lenders to find terms that fit your situation.

Elmwoodautosalesri uses the Capital One digital retail platform to deliver fast approvals and flexible credit solutions for buyers across Rhode Island. Every vehicle on the lot has passed a thorough inspection, so you are financing a car you can trust. From standard dealer loans to Buy Here Pay Here arrangements, the team matches your credit profile to the right financing path. Visit the dealership or start your application online to see what you qualify for today.

FAQ

What is dealer financing and how does it work?

Dealer financing is an indirect loan where the dealership arranges credit through a network of lenders on your behalf. You apply at the dealership, the dealer submits your application to multiple lenders, and you receive loan terms without visiting a bank.

Is dealer financing more expensive than a bank loan?

Not always. When manufacturer promotional rates like 0% APR are available, dealer financing is cheaper than any bank rate. Outside of promotions, dealers add a markup of 0–3% above the lender's approved rate, so comparing with a bank pre-approval is the best way to know.

Can Rhode Island residents with bad credit get dealer financing?

Yes. Dealers work with subprime lenders who approve buyers with FICO scores below 600, including those with recent bankruptcies or limited credit history. Buy Here Pay Here options are also available for buyers who do not qualify through standard lender networks.

How fast is dealer financing approval compared to a bank?

Dealer financing platforms like DealerTrack process approvals in minutes, often allowing same-day vehicle pickup. Bank or credit union approvals typically take 1–3 business days.

Should I get pre-approved before visiting a dealership in Rhode Island?

Getting pre-approved at a bank or credit union gives you a rate benchmark and negotiating leverage. You are not required to use it, but it protects you from accepting a dealer markup without knowing whether a better rate was available.