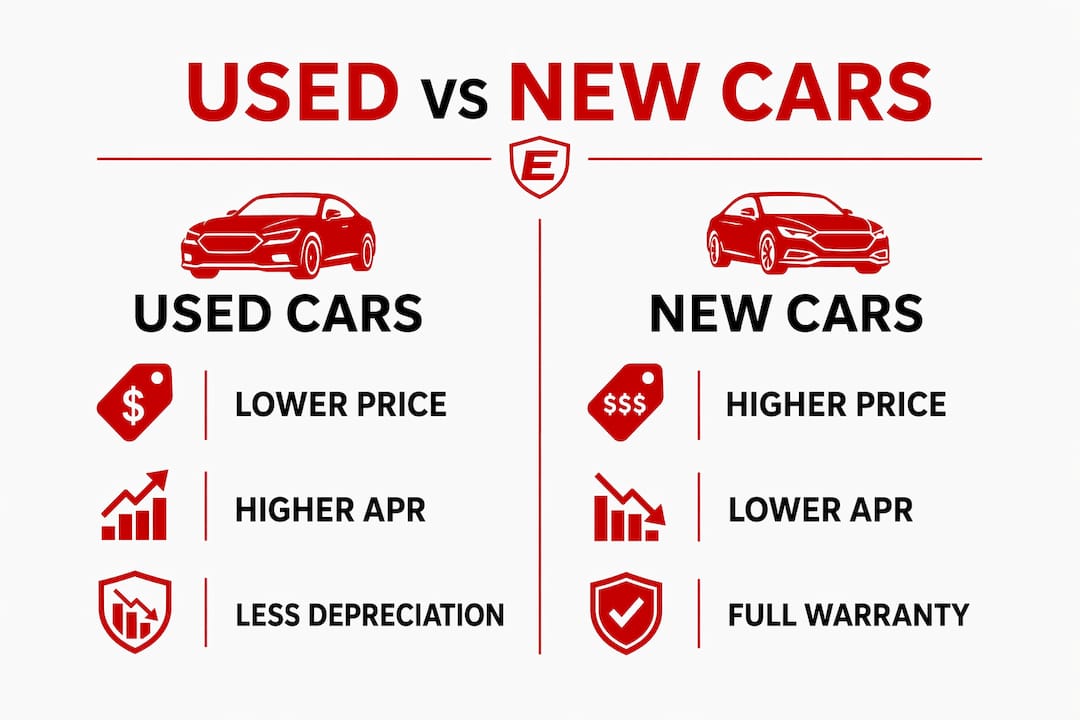

Buying a used car is the smarter financial choice for most buyers because it avoids the steepest depreciation curve that hits new vehicles the moment they leave the lot. The average new car costs $49,191 in 2026, while the average used car sells for $25,533, a difference of more than $20,000 before you factor in financing, insurance, or taxes. That gap represents real money you keep in your pocket. Understanding why buy used car over new comes down to three core factors: depreciation, total financing cost, and the reliability protections now available through certified pre-owned programs and independent inspections.

How does depreciation make used cars a better deal?

Depreciation is the single largest cost of owning any vehicle, and new car buyers absorb the worst of it. New cars lose 20 to 25% of their value in the first year alone, and roughly 50% by the five-year mark. That means a $49,000 new vehicle is worth approximately $24,500 after five years, regardless of how carefully you maintained it.

When you buy a pre-owned vehicle that is three to five years old, the original owner has already absorbed that loss. You pay a price that reflects the car's current market value, not its showroom sticker. The depreciation curve flattens significantly after year three, so your vehicle holds its value far better during your ownership period.

| Vehicle Age | Approximate Value Retained | Depreciation Absorbed by Buyer |

|---|---|---|

| Brand new (Year 0) | 100% | None yet |

| After Year 1 | 75 to 80% | 20 to 25% |

| After Year 3 | 60 to 65% | 35 to 40% |

| After Year 5 | 45 to 50% | 50 to 55% |

| Used (3 yrs old at purchase) | Stable curve | Already absorbed |

This also affects your loan balance. A lower purchase price means a smaller loan principal, which reduces the risk of going "underwater" on your financing. Resale value stays more predictable when you buy at the right point on the depreciation curve.

Pro Tip: Target vehicles that are two to four years old with under 40,000 miles. This range captures the maximum depreciation savings while still leaving significant useful life in the vehicle.

Used car sales of model year 2024 or later jumped 24% in Q1 2026, which confirms that buyers are actively recognizing this value window. Demand for near-new used vehicles is rising precisely because the price-to-quality ratio is so favorable.

What are the financing differences between used and new vehicles?

Used car loan interest rates run higher than new car rates. New car APRs average around 6.4% while used car APRs average around 11.3% as of early 2026. That spread of roughly four to five percentage points sounds alarming, but the math often still favors the used car buyer.

The reason is simple: you are borrowing far less money. A $25,000 used car loan at 11.3% over 48 months generates significantly less total interest than a $49,000 new car loan at 6.4% over 60 months. Lower principal wins over lower rate when the price gap is this large.

| Financing Scenario | Loan Amount | APR | Term | Est. Monthly Payment | Est. Total Interest |

|---|---|---|---|---|---|

| New car | $49,191 | 6.4% | 60 months | ~$960 | ~$8,400 |

| Used car | $25,533 | 11.3% | 48 months | ~$660 | ~$5,900 |

| Difference | $23,658 less | Higher rate | Shorter term | ~$300 less/mo | ~$2,500 less |

One critical nuance: manufacturer incentives like 0% APR financing or $4,000 to $6,000 cashback can sometimes close this gap on new cars. Always calculate the net cost after incentives before assuming used is cheaper on financing alone.

Pro Tip: Keep your used car loan to 48 months or fewer. Extending beyond 60 months increases total interest paid and raises the risk of owing more than the car is worth, especially on older vehicles.

The benefits of buying used car extend beyond the sticker price. Lower purchase price also means lower sales tax in most states, and insurance premiums on used vehicles are typically lower because the insured value of the car is lower. These savings compound over the life of ownership.

How do maintenance, warranties, and reliability affect used car ownership costs?

This is where the used car advantages require honest evaluation. New cars carry full manufacturer warranties and typically need only routine maintenance for the first three years. Used cars, particularly those beyond the original warranty period, can carry higher repair costs.

Used cars cost approximately $800 to $1,000 more annually in maintenance after the warranty expires compared to new cars. Over five years, that adds up to $4,000 to $5,000 in additional repair expenses. This is a real cost that belongs in any honest new vs used car comparison.

Several factors help buyers manage this risk effectively:

- Certified Pre-Owned (CPO) programs offer a manufacturer-backed warranty on used vehicles, combining used car pricing with new car assurance. CPO vehicles cover many repair costs and provide peace of mind that a standard used car purchase does not.

- Reliability ratings from Consumer Reports and J.D. Power identify which models and model years have strong long-term track records. Checking detailed reliability ratings for vehicles six to ten years old is a non-negotiable step before buying.

- Vehicle history reports from services like Carfax or AutoCheck reveal accident history, title status, and service records. A clean history report significantly reduces the risk of hidden mechanical problems.

- Pre-purchase inspections by an independent mechanic catch issues that a test drive and visual inspection miss. This step costs $100 to $150 and can save thousands in unexpected repairs.

The key insight here is that the maintenance cost gap between used and new is manageable with the right research. Buying a three-year-old Toyota Camry or Honda CR-V with a strong reliability record and a clean vehicle history report carries far less risk than buying an older vehicle with an unknown service history.

What practical tips help you maximize value when buying used?

Getting the most out of a used car purchase requires a clear process. The financial savings on used cars are real, but they depend on making informed decisions at each step.

- Get an independent pre-purchase inspection. Even when buying from a reputable dealer or a CPO program, pay for an independent inspection from a mechanic you trust. Hidden mechanical problems are the primary way used car buyers lose money.

- Target two to four year old vehicles. This age range captures the maximum depreciation savings while keeping the vehicle within a reliable service window. Models like the Honda Accord, Toyota RAV4, and Mazda CX-5 hold their reliability well into this range.

- Check the total cost of ownership, not just the sticker price. Factor in insurance, registration, expected maintenance, and financing costs. Use tools like Edmunds True Cost to Own calculator to compare specific models side by side.

- Keep loan terms short. A 48-month loan on a used car is far safer than a 72-month loan. Longer terms on older vehicles increase the chance that your loan balance exceeds the car's value before you pay it off.

- Consider time-saving car buying strategies that help you research inventory, compare prices, and secure financing before you set foot in a dealership. Preparation is the strongest negotiating tool a buyer has.

- Review insurance costs before you commit. Call your insurance provider with the VIN or at least the year, make, and model before signing. Insurance on a used luxury vehicle can sometimes exceed the savings from the lower purchase price.

The decision between used and new ultimately depends on your budget, the available manufacturer incentives, and your specific reliability needs. Used is not automatically better in every scenario, but for most buyers who prioritize financial value, the used car advantages are substantial and well-documented.

Key takeaways

Buying a used car saves most buyers over $20,000 upfront and avoids the steepest depreciation loss, making it the stronger financial choice for the majority of vehicle buyers in 2026.

| Point | Details |

|---|---|

| Upfront price advantage | Used cars average $25,533 vs. $49,191 for new, saving buyers over $20,000. |

| Depreciation timing | New cars lose 20 to 25% of value in year one; buying used means someone else absorbed that loss. |

| Financing reality | Higher used car APRs are offset by a much smaller loan principal and shorter recommended terms. |

| Ownership cost management | CPO programs, reliability ratings, and pre-purchase inspections reduce the repair cost risk of used vehicles. |

| Loan term discipline | Keeping used car loans to 48 months or fewer protects buyers from owing more than the car is worth. |

My honest assessment of the used vs. new decision

At Elmwoodautosalesri, we talk with buyers every week who come in convinced they need a new car and leave understanding why a two or three year old vehicle serves them better. The math is rarely close. When you account for the full picture, including depreciation absorbed, lower insurance, lower sales tax, and a smaller loan, the used car almost always wins on total cost.

That said, I want to be direct about when new makes sense. If you plan to own a vehicle for ten or more years, the annual depreciation cost on a new car spreads thin enough to become competitive. If you need the latest driver assistance technology or a specific powertrain that is not yet available in the used market, the premium may be justified. And if a manufacturer is offering 0% APR financing on a new model, run the numbers carefully before assuming used is cheaper.

The mistakes I see most often are buyers who stretch a used car loan to 72 months to lower the monthly payment, and buyers who skip the pre-purchase inspection to save $150. Both decisions cost far more than they save. A used car purchase done right, with a short loan, a clean vehicle history report, and an independent inspection, is one of the most financially sound decisions a buyer can make. One done carelessly can erase every dollar of the price advantage.

Research and a trusted dealership are your two best tools. Neither is optional.

— Elmwood

Find quality used cars with transparent financing at Elmwoodautosalesri

Elmwoodautosalesri makes the used car buying process straightforward and low-pressure for buyers in Providence, RI and the surrounding area.

Every vehicle on the lot goes through a thorough inspection before it is offered for sale, so you know the car meets real safety and reliability standards before you commit. Financing options include tailored solutions for a range of credit histories, including buy here, pay here programs that give more buyers access to reliable transportation. There are no commission-based sales tactics, which means the team focuses on finding the right vehicle for your needs rather than pushing the highest-priced option. Browse current inventory and financing options to start your search with confidence.

FAQ

How much cheaper is a used car compared to a new car?

The average used car costs $25,533 compared to $49,191 for a new car in 2026, a difference of more than $20,000. Additional savings on insurance premiums and sales tax widen that gap further over the ownership period.

Is a used car worth it if the interest rate is higher?

Yes, in most cases. Used car APRs average around 11.3% versus 6.4% for new cars, but the much smaller loan principal typically results in lower total interest paid and lower monthly payments overall.

What is a certified pre-owned vehicle?

A certified pre-owned (CPO) vehicle is a used car that has passed a manufacturer-backed inspection and comes with a limited warranty, offering a middle ground between standard used car pricing and new car reliability assurance.

How do I reduce repair risk when buying a pre-owned vehicle?

Order a pre-purchase inspection checklist from an independent mechanic and request a vehicle history report before signing. These two steps, costing roughly $100 to $150 combined, catch the majority of hidden mechanical problems.

What loan term should I use for a used car?

Keep the loan term to 48 months or fewer. Extending beyond 60 months on a used car increases total interest costs and raises the risk of owing more than the vehicle is worth before the loan is paid off.